Marcora for Slovenia: What are the fiscal consequences of the much-needed legislative innovation?

Elena Galevska1, Kosta Marco Juri2, and Tej Gonza3

orcid.org/0000-0001-8285-9406, orcid.org/0000-0001-7897-6271, orcid.org/0000-0002-3136-3889

Abstract

Marcora is a special model for worker buyouts that offers a variety of financial instruments and institutionalized technical assistance for a group of workers that want to continue the company’s operations. During the past 23 years, Marcora proved to be quite effective in decreasing the levels of unemployment. The proposed Marcora legislation for Slovenia suggests upfront payment of six-monthly unemployment benefits to the employees saving the business’ crisis. Comparing this amount with the cost per unemployed person in the absence of the Marcora law, we conclude that having the Marcora law would lead to lower costs, a potential annual raise of tax revenue from corporate taxation, and gains from taxes and contributions paid on wages in the Republic of Slovenia. However, to achieve the expected outcomes, the institutional investors supporting the Marcora must be adequately equipped with the means to provide the required technical, organizational, and financial assistance.

1 Marketing Manager at the Institute for Economic Democracy, Franklin Ruzvelt 58/17, 1000 Skopje, North Macedonia. 2 Researcher at the Institute for Economic Democracy, Kvedrova cesta 11, 6000 Koper, Slovenia. 3 Director at the Institute for Economic Democracy, Prvomajska ulica 15, 1000 Ljubljana, Slovenia.

Corresponding Author: Elena Galevska, Marketing Manager at the Institute for Economic Democracy, North Macedonia. Email: elena.galevska@ekonomska-demokracija.si.

I. Introduction

Employment stability and job opportunities, both high priorities of economic policies, are threatened by repeated economic crises, cost-optimization in production, and ownership succession problems in the small and medium-sized enterprise (SME) sector. Historically, governments have addressed but also reproduced unemployment (Walters, 2000). Unemployment benefits and support in the search for new employment are conventional unemployment policies; however, governments often go beyond these conventional measures to counter potential job losses. In the recent pandemic crisis that incurred deadly liquidity problems in the SME sector by restricting consumption and disrupting global distribution chains, the threat to SMEs and their employees was quite serious (Chinn et al., 2020; Juergensen et al., 2020; Kohlscheen et al., 2020).

It was a decisive intervention of the Slovenian (and other) governments that prevented – or rather interrupted – the socio-economic catastrophe, allowing us to enjoy close to record-low unemployment levels in Slovenia right now (Zaletelj et al., 2022). On the other hand, we can be justly concerned about any new interruptions to economic activity, since such strong government intervention is neither fiscally nor ideologically sustainable. Also, crises are not the only cause of unemployment. While less significant, another reason for the loss of jobs is cost-optimization, where owners of companies look for cheaper production costs abroad, closing down and severely decreasing production in Slovenia (Cerar, 2021; Masten, 2021). In 2021, we have seen quite a few examples of closing companies due to cost-optimization (Gonza et al., 2022). The third reason for job loss is the challenge of ownership succession in the SME sector, which threatens tens of thousands of jobs in Slovenia in the next decade (Duh, 2012; An SME Strategy for a Sustainable and Digital Europe, 2020; Gonza, 2020).

The loss of jobs and high unemployment numbers burden the state budget on both the expenditure side and the revenue side. On the one hand, cash inflows in form of taxes and social security benefits decrease due to the declined number of workers in the country. On the other hand, expenditures increase as the government is obligated to help those who were dismissed by paying unemployment benefits, covering health and social insurance, pension contributions, reimbursing travel costs, financing labor market activation services (Zavod RS za zaposlovanje), and undertaking other indirect costs of increased material and psychological instability of the recently unemployed. Moreover, while the unemployment benefits certainly have many positive effects for beneficiaries, like preventing the risk of poverty, allowing more time to search for decent jobs, and maintaining consumption, they can contribute to social stigma, psychological issues, and may prolong the passive condition of the unemployed (Moffitt, 2014). That’s why it is important to complement the passive strategies of taking care of the unemployed with active employment strategies.

Understanding the significance of active employment policies, some EU countries have made steps in that direction decades ago. Italy, France and Spain assist workers in the gathering of funding for recovering a distressed company, although the amounts are often insufficient. The Spanish law, Pago Unico, provides workers with the option to take three years’ worth of unemployment benefits in a lump sum, with the obligation to invest it into the capital of the cooperative or to transform the closing organization into a worker cooperative (Delgado & Claude Laliberté, 2014). There is another very important active unemployment policy in Italy, under the name Legge Marcora (henceforth ‘Marcora’). For 23 years, Marcora has proved to be quite an effective instrument when it comes to decreasing the levels of unemployment (De Berardinis, 2015). Similarly to the Spanish example, Marcora allows workers to receive unemployment benefits in lump-sum to make an asset purchase of the failing or closing company, which prevents workers from taking over the liability side of the balance sheet but only the bankruptcy estate (Carrano et al., 2017).

What are the potential fiscal consequences of the adoption of an active employment policy for the Slovenian state budget? This paper tries to answer this question by using the available data on fiscal consequences in Italy. The model assumed to be adopted is a generic Marcora concept developed in recent literature (Gonza, Berkopec, Ellerman, 2022; Gonza et al., 2021). While the study is conducted based on the information on the Slovenian SME sector and unemployment benefits, the implications are more general, since the net fiscal effect of the proposed legal framework would be similar for other countries (albeit not in terms of nominal values). In the second section, we outline the relevant information about the Italian Marcora for the purpose of this paper. In the third section, we identify the need for a Marcora-like law in Slovenia. In the fourth section, we estimate three relevant sources of fiscal consequences of the potential Marcora-like law in Slovenia. The last section concludes the paper and proposes, based on preliminary calculations of fiscal cost and other positive externalities, that the Slovenian government should indeed adopt a Marcora-like mechanism.

II. Some Preliminary Data on Italian Marcora Experience

Italy, France and Spain all offer slightly different but principally similar employment policies complementary to paying out unemployment benefits and trying to engage the unemployed through special labor activation programs. The closest and most relevant to Slovenia is the Italian Legge Marcora, a legal framework with a network of supportive institutions that assists worker buyouts (WBOs)[1]. The aid consists of financial instruments and technical mentorship for a group of workers who do not want to face unemployment and want to continue with the production within the existing or restructured business plan. Put in place in 1986, disputed by the European Commission in 1996, and passed again in 2008, the Marcora framework has assisted 301 WBOs, saved thousands of jobs and raised the added value of the businesses (Cooperazione Finanza Impresa, 2021).

Furthermore, saving jobs by providing a possibility for entrepreneurial reactivation directly to the workers of the closing companies proved to be a very profitable investment for the Italian government. According to data provided by Cooperazione Finanza Impresa (CFI)[2], which is one of the most important institutional investors established by the Marcora Law in 1986 (Carrano et al., 2017), investments in the cooperative sector between 2008 and 2017 generated a return 8.1 times greater than the initial invested capital (Mariconda, 2019). In fact, the investments amounted to € 94 million, whereas the return was € 774 million. The return has been calculated by considering (i) the expected reduction in government spending on social security, (ii) the appreciation of CFI's capital, (iii) dividends and (iv) interest income, as well as (v) increases in tax revenue. Some estimates suggest that the Marcora Law has, since its implementation in 1986, produced a return amounting to almost 28 times the invested capital (Rete Italiana Imprese Recuperate, 2021).

The process of converting closing companies into functional worker cooperatives is helped by a second-tier national institutional investor CFI, major unions, local authorities, and other national or regional consortia that finance and support WBOs (Cooperazione Finanza Impresa, 2019). CFI plays an important role in WBO creation, having intervened in 77.43 % of the 257 Italian WBOs within the Marcora framework (Vieta, 2015). Already in the first 7 years of its existence, CFI invested € 40 million in saving 89 businesses, whose turnover amounted to more than € 230 million and employed above 3,100 workers (Johnson, 1993). According to two different studies from 2015 and 2018, the overall investments are estimated to account for around € 170 million, helping create 13,000 jobs and saving approximately 300 companies (Antonazzo, 2018; De Berardinis, 2015).

Cooperatives are more likely to form within geographically immobile workforces, which are also inflexible regarding the line of business they work in. About 65.4 % of Italian WBOs operate in the manufacturing sector, while the remaining deal with transport, logistics, wholesale, and retail (Vieta, 2015). Another characteristic of WBOs is that almost all of them are SMEs, defined as organizations with up to 249 workers (Vieta, 2015). In Italy, SMEs represent 99 % of the national entrepreneurial system and contribute to approximately 30 % of GDP (Varrella, 2021).

III. Identifying the Need for Marcora-Like Law in Slovenia

What is the experience of worker groups trying to organize to purchase failing or closing companies? There are a few laws that could potentially provide a legal basis for receiving subsidies and debt capital to SMEs, for example, “Zakon o spodbujanju investicij” (Uradni list RS, št. 13/18 in 204/21) or “Zakon o podpornem okolju za podjetništvo” (Uradni list RS, št. 102/07, 57/12, 82/13, 17/15, 27/17 in 13/18 – ZSInv). However, the experience shows that neither has proved useful in addressing practical problems that workers face when businesses are shutting doors (Gonza, Berkopec, and Ellerman, 2022).

In the case of failing Fructal Ajdovščina d.o.o., a group of workers organized through a formal initiative called Novi Fructal and managed to collect € 8 million in warranties, but the initiative remained € 12 million short of the required € 20 million to purchase the bankruptcy estate. Since the deadlines were short and the government did not have a mechanism to support them, the initiative ultimately lost against the bid of the Serbian corporation Nectar Group in 2011, which immediately undertook a job dismissal spree, firing more than 100 workers to attain higher “profitability of operation” in the next three years. A similar situation could be observed when Novoles d.o.o. registered insolvency in 2011. After the bankruptcy, a group of twelve workers organized a cooperative Novi Novoles but failed to attain a loan due to the relatively low value of equity capital in the cooperative. Since the cooperative did not manage to receive any aid from the government and the banks were not willing to find a solution, the bankruptcy estate of Novoles d.o.o. was purchased by Metalka Commerce and more than 400 workers lost their jobs. There are other very similar and more recent examples (Sanitec d.o.o., Armal d.o.o., Adria Airways Tehnika, M-Tom d.o.o., etc.), where very ambitious workforces faced severe financial constraints and lack of technical assistance to purchase the bankruptcy estate and continue with production.

Lately, we have witnessed a few cases where owners simply decided that Slovenian workers are too expensive due to labor regulation and corresponding taxes. In 2021, there were three cases where owners announced massive job losses (Safilo d.o.o., Adient Slovenj Gradec, Treves d.o.o.), while Revoz d.d. has also recently announced that it is restructuring and letting go more than 400 workers in 2022. Most of the examples above show that there is a systematic aversion of the private financial sector to support workers’ initiatives for taking over the companies that are going under or closing doors due to other reasons. While the Slovenian Developmental Bank should work to bridge market gaps, our collaboration with the bank proved that it holds an irrationally conservative attitude towards inclusive ownership structures even if based on good international practice.

Past cases, some of which are mentioned above, indicate that there is an absence of appropriate legal mechanisms providing workers with financial and technical assistance to prevent mass dismissals in Slovenia. SMEs represent 99.8 % of the non-financial business economy in terms of the number of enterprises (SURS, 2019), contributing to 64.5 % of value-added and 72 % of employment, putting Slovenia above the EU averages (European Commission, 2019). In addition to the high relative presence of SMEs in Slovenia, most of these operate in sectors especially suitable for WBOs, with 50.2 % of all SMEs accounting for 44.7 % of SME employment operating in wholesale, retail, and manufacturing (European Commission, 2019). Combined with the relatively immobile workforce and the economic downturn upon the expected fiscal and monetary restriction, we estimate that the demand for a Marcora-like law will be high in the future. In the next section, we analyze the expected fiscal consequences of such a law.

IV. Expected Fiscal Consequences for the Slovenian State Budget

To evaluate the potential for fiscal consequences, data on the number of SMEs (excluding micro-companies) that filed for bankruptcy in 2017 in Slovenia – namely 181 – will be used (SiStat, 2021; Statista, 2021). Having in mind that the average size of Italian WBOs is 41 workers (Vieta, 2015), while the average size of an Italian SME is 26 employees (ISTAT, 2021), we come to the conclusion that WBOs are, on average, 36.59 % larger than SMEs. Given that the average Slovenian SME consists of 33 employees (Močnik et al., 2019), it can be assumed that a Slovenian WBO would include 45 workers. The average number of workers in SMEs and the number based on the Italian experience provide the range for evaluating the number of beneficiaries, which is between 5,973 beneficiaries and 8,158 beneficiaries.

These numbers are underestimated in some respects and overestimated in others. The estimates do not include jobs lost due to companies moving their business abroad for cost optimization, nor do they include estimates of job losses due to ownership succession challenges. On the other hand, the extrapolation of the average size of a WBO from the Italian experience may be problematic since it is based on small sample size. The total number of WBOs from 2008 to 2018 in Italy is just above 100 and the total number of companies financed by CFI since its establishment is 536, out of which 301 are WBOs (Cooperazione Finanza Impresa, 2021; De Berardinis, 2018). Therefore, a more conservative scenario for the average size of WBO will be constructed, which will be based on the average size of SMEs in Slovenia. It is also important to emphasize that our evaluations are estimates of the potential if all the workers of companies that file for bankruptcy would use the Marcora framework. Thus, the reality is somewhere between the calculated potential and the status quo. Finally, for the cases where we needed to evaluate the indirect benefits of employee ownership, we considered empirical research on international employee-ownership practice.

Estimate of Decreased Expenditure

To estimate the potential state budget savings, we need a range of potential beneficiaries and a variety of other information, like direct costs (unemployment benefits, health and social insurance, pension contributions, travel costs reimbursement, the cost of labour market activation services etc.), indirect costs (costs of psychological instability, increase in criminal activity due to material insecurity, the negative effects of increased unemployment rates on local communities etc.), and opportunity costs (loss of productive activity and taxes collected). Most of these costs are rather difficult to find or calculate, and for that reason, the estimate will necessarily be undervalued.

Starting with direct costs, in Slovenia, the monthly unemployment benefits per person vary between € 530.19 and € 892.00 (European Commission, 2022; Zavod Republike Slovenije za Zaposlovanje, 2021). Given that these amounts decrease over time and are influenced by the prior employment length and the amount of the wage received, assessing the payments per person according to the current legislation is rather difficult. In 2019, Slovenia allocated € 240 million for the unemployment benefits while the number of beneficiaries of unemployment benefits was 46,000 (Tomažič, 2020), which equals € 5,217.39 per person. Though this calculation could be used as the basis for the analysis, we searched for a value that we believe would be more realistic. Such value needs to reflect also the fact that the model considered proposes a lump-sum payment of the six-month-worth of unemployment benefits in advance (Gonza, Berkopec, Ellerman, 2022; Gonza et al., 2021). Hence, we used the average amount of unemployment benefits paid out in November 2021, amounting to € 764.15 (Zavod Republike Slovenije za Zaposlovanje, 2022a). With this basis, we estimate that the Slovenian government would spend € 4,584.90 per beneficiary under the proposed Marcora-like law.

Next, the opportunity costs which include the preservation of tax revenue caused by the preservation of jobs should be estimated. More specifically, it is necessary to assess the tax revenues from the income tax and the value-added tax, which will be preserved if job losses are prevented. Taking into consideration that the average income tax rate in Slovenia is 34.7 %, and the average salary in the private sector amounts to € 1,765.35 in 2021, every worker whose job is saved thanks to the Marcora framework would contribute to state savings of € 7,350.92 per year. The standard value-added tax in Slovenia is 22%, while the reduced rates are 9.5% and 5%. If we consider a 20% value-added tax and the average value-added per employee in the Slovenian SME sector, which amounts to € 42,000.00 per year, it means that each worker contributes € 8,400.00 per year to the state budget through value-added tax. The opportunity cost is therefore estimated at € 15,750.92 per worker. Combined with the direct cost of € 5,217.39 and neglecting other indirect costs mentioned above, the total cost for the state budget per unemployed person in absence of the Marcora framework is € 20,968.31. Comparing this amount with the € 4,584.90 (which includes the payment of the amount of six-monthly unemployment benefits upfront), it becomes obvious that having the Marcora law would lead to 4.57 times lower cost for the Republic of Slovenia.

Consequently, in case of the adoption of the law, the state budget saves € 16,383.41 per person on an annual basis. Having this data, the potential savings can be calculated by multiplying by the number of potential beneficiaries of the Marcora framework. Namely, considering both the conservative estimate of the company size and the optimistic assessment of the number of workers in a typical Marcora enterprise, the estimated potential savings for the state budget range from € 97,858,107.93 to € 133,442,874.45 per year.

Another approach to assessing the savings for the state budget of the Republic of Slovenia would be relying on the data from Italy as a reference. This is best done by comparing the average state costs per beneficiary under the Marcora act with the average state costs per unemployed worker, including the indirect and opportunity costs. According to the Italian experience, worker buyouts are expected to generate higher tax revenues and require lower investments. The financial resources per worker amount to € 14,000 since the inception of the Marcora Law, compared to the average of € 40,000 out of public contributions for unemployment benefits per worker (Carrano et al., 2017; Lomuscio & Salvatori, n.d.; Mori et al., 2008). Undoubtedly, this data provides great support in favor of worker cooperatives, indicating that introducing the appropriate legislation can lead to 2.86 times bigger state savings per potential unemployed person. Taking the data on the average expenditure for a potentially unemployed person within the Marcora act for Slovenia and the factor of budget savings in Italy, we can conclude that the annual cost per unemployed person in Slovenia is € 13,112.81. Furthermore, the savings for the state budget per one beneficiary of the proposed Marcora law is € 8,527.91. Multiplying the calculated amount with both the conservative and optimistic estimates of beneficiaries, we find that the potential range of savings for the Republic of Slovenia is between € 50,937,230.32 and € 69,570,689.78.

The former Italian Minister of Economic Development, Federica Guidi, stated that, besides helping reduce unemployment benefit costs, the national institutional investors have also successfully managed to protect and generate jobs and to create value and new investments. More precisely, the savings that Cooperazione Finanza Imprese (CFI) has generated by not allocating unemployment benefits are estimated to account for € 113 million in the period between 2006 and 2012 (Antonazzo, 2018). Finally, the cooperatives faced only a 10 % failure rate during the first 7 years of Marcora’s implementation (Johnson, 1993), while only 12.8 % WBOs created in the period after 2009 have failed (Vieta, 2015), indicating positive survival rates, and demonstrating that the model is very successful in saving jobs and companies, especially in times of crisis and austerity (CECOP-CICOPA, 2012b, 2013; Zevi et al., 2011).

Other Drivers of the Increase in Tax Revenue and Financial Income for the State

The Italian legislation promotes WBOs and co-op start-ups by allowing employees of companies in crisis (be it because of insolvency or succession problems) and unemployed people to capitalize – in a lump-sum – the unemployment benefits they are entitled to and by granting them access to 'soft financing' (Carrano et al., 2017). This allows employees to save their companies and keep production going, which – all things being equal – has a short-term positive effect on the government budget, as the tax base is prevented from shrinking. Moreover, since WBOs are significantly more longevous than the average company (Mariconda, 2019), the long-term effects in terms of tax revenue are expected to be positive as well.

According to data provided by CFI, the 85 companies which were involved in CFI-financed WBOs between 2012 and 2019 not only continued to perform as well as before but rather more than doubled their revenue, which increased by 102 % and increased the number of employees by 22 % (Cooperazione Finanza Impresa, 2021). While it might be unrealistic to expect Slovenian WBOs to perform as well as the companies financed by CFI did during the course of the last decade, there is still plenty of evidence suggesting that employee-owned companies perform better than average ones. This is particularly true for WBOs since employees are incentivized to save their companies only when they recognize that there is a ‘healthy core’ worth saving - something which might also explain the strong economic performance of Italian WBOs.

A study commissioned by the Region of Tuscany (one of the Italian regions with the highest number of WBOs) (Vieta, 2015) to assess the impact of public investments in worker-owned companies made between 1986 and 2001 (many of which fall under the Marcora framework), shows that the majority of employee-owned companies have witnessed an increase in revenue following the intervention of publicly funded institutional investors (Mori et al., 2008). Data from the US show that employee-owned companies which take the form of ESOPs are, on average, between 4 % and 10 % more productive than their non-ESOP counterparts (Blasi et al., 2013; Brill, 2012; Freeman, 2007; Kruse, 2016). Moreover, a report commissioned by the European Commission concluded “that financial participation [of employees] has a positive or neutral effect on productivity” (European Federation of Employee Share Ownership, 2019). Consequently, not only is it reasonable to expect a Marcora-inspired law to increase tax revenue because it would allow financed companies to continue to operate as usual, but also because of the positive effect it would have on their overall performance.

Since it is impossible to anticipate how many companies will be converted into WBOs as a result of a Marcora-inspired law, we are only able to provide an estimate of the potential increase in tax revenue that would result from the measure. Hence, the conclusions will be based on the average performance of SMEs, thus leaving the positive impact of employee ownership on business performance out of the equation. According to data from 2017, the average value added per SME amounts to roughly € 1,400,000, while the profitability is approximately 39 %. On the basis of the effective tax rate (13.1 %), we estimate that every saved company will pay around € 71,256 in corporate taxes per year. Therefore, the tax revenue raised from corporate taxation is expected to increase up to € 12,946,206 per year, depending on the number of WBOs. On the basis of the average tax rate and the rate of contributions on wages (34.7 %), the average number of employees in an SME (33) and the average gross wage in the Slovenian private sector in 2021 (€ 1,765.35), it appears that tax revenues raised from taxes and contributions paid on wages may increase up to € 43,907,030 per year, depending on the number of WBOs.

We also anticipate an increase in VAT revenue. Given that the average value added per year of an SME employee is approximately € 42,000, we can assume that the total value-added, created by 181 companies in a year, amounts to € 250,866,000. The standard VAT rate in Slovenia is 22 %, while the reduced VAT rates are 9,5 % and 5 %. Therefore, the estimated increase of tax revenue raised from VAT is calculated by applying a 20 % tax rate to the total value added of 181 companies. Thus, it is expected that the tax revenue raised from VAT increases up to € 50,173,200 per year, depending on the number of WBOs.

A Marcora-inspired law would also increase tax revenue raised from VAT by allowing employees to stick to their consumption habits. Assuming that salaries remain unaltered after a company is converted into a WBO, it is reasonable to expect employees of converted companies – who would not see their disposable personal income being reduced – to consume more than they would in case unemployment benefits were their main source of income.

Moreover, employee-owned companies are significantly less prone to relocate to other countries in pursuit of lower taxes and/or to cut labor costs, as they operate in the interest of employees and of the local communities more broadly. Thus, increasing the number of employee-owned companies by promoting WBOs and creating a fertile ground for employee-owned start-ups, while also keeping already-existing cooperatives sound, is an effective strategy to preserve domestic ownership and limit capital outflow. By doing so, public authorities can make sure that capital income fuels domestic consumption instead of being moved abroad, which should result in an increase in VAT revenue.

Finally, there is an increase in the financial income of the state budget. Soft financing provided to the cooperative sector has proven to be a good investment for the Italian state. CFI makes use of multiple modes of financing to invest in cooperatives, which take the form of both debt and venture capital. According to data provided by CFI, the interest income and dividends earned by CFI between 2008 and 2017 amount to € 4 million. During this period, CFI invested € 94 million in the Italian cooperative sector (Mariconda, 2019). While a similar return – especially as far as dividends are concerned – might be overstated due to the exceptional performance of WBOs financed by CFI between 2012 and 2019, there is no reason to believe that the earnings constituted by interest income and dividends per financed company will be drastically lower, given the longevity and sound economic performance typically associated with WBOs and employee-owned companies in general.

Estimate of Direct Costs

With the introduction of the Marcora Law in Italy, two public funds were established to offer financial support to the cooperative sector. The Fondo di rotazione per la promozione e lo sviluppo della cooperazione (also known as Foncooper[3]), managed by Banca Nazionale del Lavoro and the Special fund, controlled by CFI. While the first aims at promoting the general development of the Italian cooperative sector by providing debt capital under favorable conditions, the second acts as a “vanguard of financing and supporting Italy’s WBOs” (Vieta, 2015) by making use of both debt and venture capital and by providing companies with technical and organizational assistance. Of paramount importance for the success of the Marcora framework is also the highly developed Italian cooperative movement, which greatly supports newly established cooperatives (Vieta, 2015).

For the proposed legislation to achieve its expected outcomes, it must be ensured that the institutional investors supporting the legislative framework are adequately equipped with the means to (A) actively promote WBOs as a solution to business crises by establishing initial contact with potentially interested parties and (B) provide employee-owned companies (particularly WBOs) with the technical, organizational, and financial assistance needed to successfully operate on the market, as well as to support them in gaining access to external financing (Cooperazioe Finanza Impresa, 2014). We propose to organize public intervention in support of the employee-owned sector as follows:

1. Activities regarding the financing of the employee-owned sector, as well as the technical and organizational assistance, would be taken over by the Slovenski Podjetniški Sklad (SPS). The Marcora framework has as a part of its backbone one national institutional investor – CFI –, which was established ad hoc for dealing with the Italian cooperative sector and for actively promoting WBOs. For this reason, we believe it would be necessary to supplement the already-existing departments of SPS with a new department inspired by CFI, which would be formed by two sub-departments. Said sub-departments would each emulate one of CFI's four bodies, with one being responsible for activities of promotion and investigation and the other dealing with implementation and monitoring. Said activities require a high degree of expertise in employee-owned companies and WBOs and can hardly be taken over by SPS in its current state. CFI currently employs eight people (out of a total of fourteen) who deal with the abovementioned activities (Cooperazioe Finanza Impresa, 2020). We estimate that the total number of employees working in the Slovenian equivalents of these departments should amount to a minimum of five and a maximum of ten employees. These figures have been to a certain extent chosen arbitrarily after taking into consideration the specificities of the Slovenian context, i.e. the significantly smaller size of its economy compared to Italy’s and the absence of a strong cooperative movement. Such a department would be tasked exclusively with providing employee-owned companies with the necessary technical, organizational, and financial support, as well as with promoting WBOs and monitoring the Slovenian business sector to intercept potentially interested companies.

2. Credit guarantee schemes could be provided by the Slovenska Izvozna in Razvojna Banka and/or Podjetniški sklad without the need for defining special financial instruments.

The organizational, professional, and administration services costs depend mostly on the training and addition of specialist personnel to SPS (or any other existing institution). Should the number of employees increase by ten units due to the creation of new departments, we estimate that the additional yearly costs associated with professional services, administration and organization would amount to roughly € 400,000. The figures have been calculated by looking at the average expenses (wages and other personnel costs, social security contributions) directly associated with each SPS employee (Slovenski Podjetniški Sklad, 2020). In addition to this, the professionals should have the relevant expertise in economic democracy and worker ownership, which means that additional costs may arise as a result of bringing the know-how to Slovenia and financing an educational program. Other unanticipated costs may also arise as a result of very high demand or due to the lack of experience of Slovenian public institutions in dealing with employee-owned companies. Therefore, our estimate should be considered as a minimum.

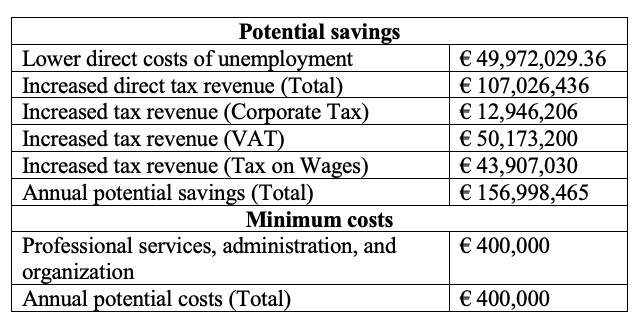

V. Conclusion The aim of this analysis was to evaluate the potential costs and benefits for a Slovenian state budget associated with the adoption of a legislative and institutional framework similar to the Italian 49/1985 ‘Marcora’ Law. The analysis mainly focused on the effects of the Marcora Law on the Italian State budget, although relevant data from other countries were used as well. The calculations in this study provide plentiful evidence of the overwhelmingly positive impact of the Marcora-like law on the Slovenian state budget, as shown in Table 1 below.

Table 1: Estimate on annual budget effects in the case of Marcora-like law adoption in Slovenia

Note: The table does not consider the anticipated increases in indirect tax revenue. Source: Author’s own elaboration.

In addition to the positive effects presented above, WBOs positively affect the state budget by creating more resilient, profitable, and both socially and environmentally responsible economic enterprises. Financial assistance to employee-owned companies has proved to be a sound investment for the state, as it produces direct returns as well as returns deriving from multipliers associated with employee ownership. Moreover, the proposed legislation acts countercyclically, improving state balances’ shock absorption when it is needed the most, namely during times of economic crisis. Employee-owners in the USA were 20 to 50 % less likely to be laid off during the 2009-2013 recession (NCEO, 2019), and a similar effect of employee ownership was found in Europe. Namely, in the UK, the sales growth of employee-owned companies increased by 11.08 %, whereas the one of the traditionally owned companies showed only 0.61 % growth during the 2008-2009 crisis (Gonza, 2020). When unemployment reached 11.2 % in Italy, between 2011 and 2012, cooperatives created approximately 36,000 new jobs (Gonza, 2020). It has been observed that the number of beneficiaries increases with the decrease in macroeconomic well-being (Vieta, 2019). According to previous research, market difficulties create a fertile ground for WBOs (Vieta, 2015). Therefore, this mechanism could be seen as an automatic fiscal stabilizer.

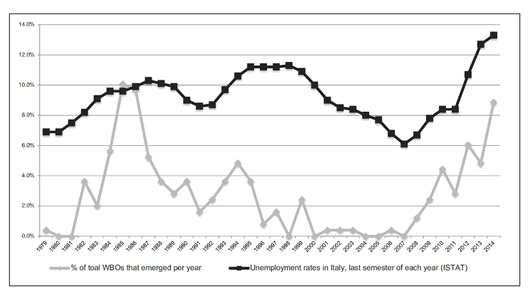

Figure 1: The Emergence of WBOs in Italy Compared with Unemployment Rates during the Marcora Law Era

Source: (Vieta, 2019).

Co-operatives have proven to increase collected taxes through positive externalities and other economic multipliers (Delgado & Claude Laliberté, 2014). The statistics for the 17-year-period between 1990-1999 and 2008-2014 show that while the average birth rate of Italian WBOs is quite similar to the average birth rate of Italian manufacturing companies (7.3 % and 7.5 % respectively), there are significant differences in the death rates – with WBOs averaging 4 % and the non-employee-owned firms, 6.5 % (Vieta, 2015). Therefore, traditionally owned companies have a 62.5 % lower probability of survival. The data is even more convincing for the period between 2007 and 2013. Namely, in this period, the average survival rate of all Italian companies under 3 years of age was 48.3 %, whereas the same indicator for the Marcora companies under 3 years of age was as high as 87.2 % (CECOP-CICOPA, 2015). Moreover, the fact that WBO creation is countercyclical is best observed when considering the times of crisis, i.e., the period between 2010 and 2014. Throughout these 4 years, the average birth rate of WBOs increased to 12.13 %, while the death rate decreased to 3.35 %, resulting in a net average growth rate of 9.21 % (Vieta, 2015). Furthermore, the cooperative sector created 36,000 jobs in 2012, when the Italian economy was hit hardest by the crisis (CECOP-CICOPA, 2012a).

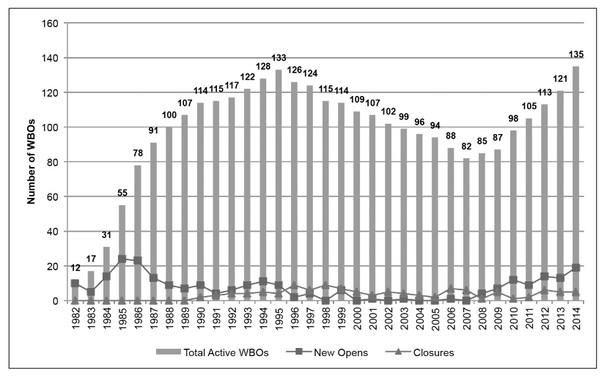

Based on the fiscal analysis presented in this paper, the adoption of the Marcora-like law in Slovenia would have a positive effect on the Slovenian state budget. Once the described legislative framework comes into force, the number of cooperatives should gradually start increasing. It is expected that the pace of cooperative creation will accelerate once the model becomes better known and there is a good practice within the country. The Italian experience also shows that WBO creation increases after the law is passed, which can be seen both after the law's adoption in 1985 and 2008 (figure 2) (Vieta, 2015).

Figure 2: Active WBOs per year in Italy Compared with WBO openings and closings per year (1979-2014

Source: (Vieta, 2015).

In addition to positive fiscal consequences, the law would have a lot of other tangible and intangible positive effects for workers, local communities, and the Slovenian economy as a whole. In that context, the authors encourage the Slovenian government to pass the needed law and allocate public finance, which would assist groups of workers to organize, reorganize, and purchase assets of failing or closing companies.

References

Antonazzo, L. (2018). Cooperation against capitalism’s biases. Workers-Recuperated Enterprises in Italy during the Great Recession. University of Salento. Blasi, J., Kruse, D., & Weltmann, D. (2013). Firm survival and performance in privately held ESOP companies. In Sharing Ownership, Profits, and Decision-Making in the 21st Century (pp. 109–124). Emerald Group Publishing Limited. Brill, A. (2012). An Analysis of the Benefits S ESOPs Provide the US Economy and Workforce. Matrix Global Advisors, Washington, DC, Available at: Https://Community-Wealth. Org/Sites/Clone. Community-Wealth. Org/Files/Downloads/Paper-Brill. Pdf (Accessed July 24, 2018). Carrano, A., Depedri, S., & Vieta, M. (2017). The Italian Road to Recuperating Enterprises and the Legge Marcora Framework: Italy’s Worker Buyouts in Times of Crisis (Research Report N.015). European Research Institute on Cooperative and Social Enterprises. https://www.euricse.eu/publications/italys-worker-buyouts-in-times-of-crisis/ CECOP-CICOPA. (2012a). 36,000 new jobs were created in Italian cooperatives in 2012. Europe. CECOP-CICOPA. (2012b). CECOP position on EC’s Green Paper: Restructuring and anticipation of change: What Lessons from Recent Experience? The European Confederation of Cooperatives and Worker-Owned Enterprises Active in Industries and Services. CECOP-CICOPA. (2013). Business transfers to employees under the form of a cooperative in Europe. The European Confederation of Cooperatives and Worker-Owned Enterprises Active in Industries and Services. CECOP-CICOPA. (2015). Workers buy-out: 30 years creating wealth in Italy. Cerar, G. (2021, November 3). V Ormožu bodo zaprli tovarno očal, delo bo izgubilo 557 delavcev. MMC RTV SLO. https://www.rtvslo.si/gospodarstvo/v-ormozu-bodo-zaprli-tovarno-ocal-delo-bo-izgubilo-557-delavcev/572563 Chinn, D., Klier, J., Stern, S., & Tesfu, S. (2020). Coronavirus (COVID-19): SME policy responses. McKinsey & Company. http://www.oecd.org/coronavirus/policy-responses/coronavirus-covid-19-sme-policy-responses-04440101/#section-d1e258 Cooperazioe Finanza Impresa. (2014). Modalità di intervento CFI: Foglio informativo. http://www.cfi.it/public/wp-content/uploads/2015/06/modalita-intervento.pdf Cooperazioe Finanza Impresa. (2020). “Costi del personale 2020.” https://www.cfi.it/upload/web_comp/add/doc/000000259_1613991482.pdf Cooperazione Finanza Impresa. (2019). CFI Incorpora SOFICOOP e Diventa L’unica Societa’ Finanziara. https://www.cfi.it/upload/web_news/11_5_000000278_1557240466.pdf Cooperazione Finanza Impresa. (2021). Workers buyout: Le coop resistono e raddoppiano il fatturato. https://www.cfi.it/upload/web_news/11_5_000000424_1626955835.pdf De Berardinis, C. (2015, September 22). The Marcora Law: An effective tool of active employment policy. Coop News. https://www.thenews.coop/98000/sector/retail/marcora-law-effective-tool-active-employment-policy/ De Berardinis, C. (2018). Workers buyout, quando il lavoro nasce da un fallimento [MorningFUTURE]. https://www.morningfuture.com/it/2018/08/31/wbo-workers-buyout-cooperative-lavoro/ Delgado, N. D., & Claude Laliberté, P. (2014). Job preservation through worker cooperatives: An overview of international experiences and strategies. International Labour Organization. http://www.ilo.org/wcmsp5/groups/public/@ed_dialogue/@actrav/documents/publication/wcms_312039.pdf Duh, M. (2012). Family Business: The Extensiveness of Succession Problems and Possible Solutions. In Entrepreneurship: Gender, Geographies and Social Context. BoD – Books on Demand. Employee buyout. (2019, June 8). European Foundation for the Improvement of Living and Working Conditions. https://www.eurofound.europa.eu/observatories/eurwork/industrial-relations-dictionary/employee-buyout European Commission. (n.d.-a). 2019 SBA Fact Sheet—Slovenia. Retrieved December 30, 2021, from https://ec.europa.eu/docsroom/documents/38662/attachments/26/translations/en/renditions/native European Commission. (n.d.-b). Slovenia—Unemployment benefits. Retrieved January 10, 2022, from https://ec.europa.eu/social/main.jsp?catId=1128&langId=en&intPageId=4785 An SME Strategy for a sustainable and digital Europe, no. COM(2020) 103 final, European Commission (2020). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM%3A2020%3A103%3AFIN European Federation of Employee Share Ownership. (2019). Employee Share Ownership The European Policy. http://www.efesonline.org/LIBRARY/2018/Employee%20Share%20Ownership%20--%20The%20European%20Policy.pdf Freeman, S. F. (2007). Effects of ESOP adoption and employee ownership: Thirty years of research and experience. Gonza, T. (2020). Employee-Owned Firms: The Multiciplicity of Crisis, Resilience, and Social Responsibility. In The Virus Aftermath: A Socio-Economi Twist (1st ed., pp. 401–420). Časnik Finance, 2020. Gonza, T., Berkopec, G., Ellerman, D., & Žgank, T. (2021). Marcora for Europe. European State Aid Law Quarterly, 1(2021). ISTAT. (2021, November 5). [Database]. http://dati.istat.it/viewhtml.aspx?il=blank&vh=0000&vf=0&vcq=1100&graph=0&view-metadata=1&lang=it&QueryId=20771&metadata=DICA_ASIAUE1P Johnson, T. (1993). The Marcora Law - Multiplying the employees’ stakes. https://www.wikipreneurship.eu/index.php/Marcora_Law Juergensen, J., Guimón, J., & Narula, R. (2020). European SMEs amidst the COVID-19 crisis: Assessing impact and policy responses. Journal of Industrial and Business Economics, 47(3), 499–510. https://doi.org/10.1007/s40812-020-00169-4 Kohlscheen, E., Mojon, B., & Rees, D. (2020). The macroeconomic spillover effects of the pandemic on the global economy. https://www.bis.org/publ/bisbull04.htm Kruse, D. (2016). Does employee ownership improve performance? IZA World of Labor. https://doi.org/10.15185/izawol.311 Lomuscio, M., & Salvatori, G. (n.d.). A Co-operative Recovery: Learning lessons from Italy’s Marcora. Retrieved September 30, 2021, from https://party.coop/cooprecovery/read/5 Mariconda, M. (2019, July 12). ’CFI strumento finanziario e di politica del lavoro per la nascita di nuove imprese e l’occupazioe. https://www.centrostudi.cisl.it/attachments/article/471/Montepulciano_cfi_mariconda.pdf Masten, A. (2021, June 28). Adient začel vročati odpovedi pogodb o zaposlitvi. MMC RTV SLO. https://www.rtvslo.si/gospodarstvo/adient-zacel-vrocati-odpovedi-pogodb-o-zaposlitvi/585815 Močnik, D., Duh, M., Crnogaj, K., Rebernik, M., & Sirec, K. (2019). Slovenska Podjetnška Demografija in Prenos Podjetij: Slovenski podjetniški observatorij 2018. Moffitt, R. (2014). Unemployment benefits and unemployment. IZA World of Labor. https://doi.org/10.15185/izawol.13 Mori, P. A., Belletti, G., & Cioni, M. (2008). L’impatto Economico dei finanziamenti pubblici sui principali settori del sistema toscano delle cooperative: Evoluzione e valutazione. Osservatorio Regionale Toscano sulla Cooperazione. https://www.regione.toscana.it/documents/10180/70188/Impatto%20economico%20finanziamenti%20pubblici_78668/dce7c0b8-8ff6-4a16-814a-2e6887d939ee Rete Italiana Imprese Recuperate. (2021). Rete italiana imprese recuperate. https://impreserecuperate.it/il-collettivo/ SiStat. (2021, November 5). Statistical Office of the Republic of Slovenia. https://pxweb.stat.si/SiStatData/pxweb/en/Data/-/1418402S.px/table/tableViewLayout2/ Slovenski Podjetniški Sklad. (2020). Letno Poročilo 2020. http://podjetniskisklad.si/images/letnaporocila/Letno-poroilo-2020.pdf Statista. (2021, January 26). Annual number of insolvent companies in Italy from 2009 to 2017. https://www.statista.com/statistics/809209/company-insolvencies-in-italy/ SURS. (2019). Mikro-, majhna in srednje velika podjetja (MSP). https://www.stat.si/StatWeb/File/DocSysFile/11018/slo-mala-srednja-podjetja.pdf Tomažič, M. (2020, April 20). Labour Force Survey Results, Slovenia, 2019. SURS. https://www.stat.si/StatWeb/nk/news/Index/8762 Varrella, S. (2021, October 12). Contribution of small and medium enterprises (SMEs) to the increase in GDP* in Italy from 2009 to 2017, by company size. https://www.statista.com/statistics/1018559/contribution-of-smes-to-the-increase-in-gdp-in-italy/ Vieta, M. (2015). The Italian Road to Creating Worker Cooperatives from Worker Buyouts: Italy’s Worker-Recuperated Enterprises and the Legge Marcora Framework (No. 78/15). Euricse Working Papers. Vieta, M. (2019). Saving Jobs and Businesses in Times of Crisis. In Cooperatives and the World of Work (1st Edition). Walters, W. (2000). Unemployment and Government: Genealogies of the Social. Cambridge University Press. Zaletelj, T. O., Rojc, N., & Vratanar, H. (2022). Labour Force Survey Results, Slovenia, 3rd quarter 2021. SURS. https://www.stat.si/StatWeb/en/News/Index/9979 Zavod Republike Slovenije za Zaposlovanje. (n.d.-b). Unemployment benefit. Retrieved September 10, 2021, from https://english.ess.gov.si/jobseekers/unemployment_benefits Zavod Republike Slovenije za Zaposlovanje. (2022a). Pravica iz zavarovanja. https://www.ess.gov.si/trg_dela/trg_dela_v_stevilkah/pravica_iz_zavarovanja Zevi, A., Zanotti, A., Soulage, F., & Zelaia, A. (2011). Beyond the Crisis: Cooperatives, Work, Finance. Generating Wealth for the Long Term. CECOP Publications.

[1]Worker buyout – is a “restructuring process in which employees buy a majority or total ownership stake in their own company and, in effect, become the owners” (Eurofound, 2019). The proposed legislation would allow employees to buy out exclusively the assets of their company, without inheriting the debts of the previous owner.

[2]Cooperazione Finanza Impresa – is an institutional investor established by the Marcora Law in 1986 “to coordinate and facilitate the financing of cooperatives within the Legge Marcora framework” (Carrano et al., 2017). Since its incorporation of SOFICOOP – the second institutional investor established by the Marcora Law – in 2020, it is the only national institutional investor currently operating under the Legge Marcora framework. It manages the public fund Fondo speciale per gli interventi a salvaguardia dei livelli di occupazione (known as Special fund).

[3]Fondo di rotazione per la promozione e lo sviluppo della cooperazione – is a rotating fund “consisting of low-interest loans and accessible to cooperatives motivated to generate or improve employment levels or productivity and for increasing or modernizing production equipment, technical services, sales, and administration” (Carrano et al., 2017). It is managed by administrative regions and Banca Nazionale del Lavoro (BNL).